Ben Mauldin | Dec 06 2025 17:08

A Special Enrollment Period (SEP) lets you enroll in ACA-compliant health coverage outside the annual Open Enrollment when you experience certain qualifying life events, such as losing employer coverage, getting married, or moving to a new service area. This article explains what a SEP is, how it differs from the Open Enrollment Period, which qualifying life events for health insurance trigger eligibility, what documentation you need, and how deadlines like the January 15 ACA deadline and ACA enrollment deadlines 2026 interact with SEP windows. Many people face gaps in coverage after a job loss or life transition; understanding SEPs prevents unintentional uninsured periods and ensures timely access to subsidies and cost-sharing reductions. You will learn step-by-step how to apply for a Special Enrollment Period through the Health Insurance Marketplace, what coverage start dates to expect, and how to choose a plan that balances premiums, provider access, and subsidy eligibility. The guide also covers less-common scenarios—Medicaid loss SEP, citizenship changes, incarceration release, and tribal-member situations—plus practical checklists and documentation examples to speed verification and enrollment.

What Is a Special Enrollment Period and How Does It Differ from Open Enrollment?

A Special Enrollment Period (SEP) is a time-limited window that permits enrollment in Marketplace coverage after certain qualifying life events, while the Open Enrollment Period (OEP) is the general annual window for anyone to enroll without a qualifying event. The SEP mechanism exists because life changes alter eligibility or create urgent need for coverage; as a result, SEPs are triggered by events rather than calendar timing, and they typically allow a 60-day special enrollment period to complete enrollment. This entity-to-entity relationship—Qualifying Life Event → Triggers → SEP access—explains why SEPs focus on eligibility triggers rather than broad access. Understanding these differences helps consumers know when to act and which documentation to gather, reducing delays during pre-enrollment verification. The next section outlines what qualifies as a Special Enrollment Period under the ACA and groups common events into practical categories so you can identify your eligibility quickly.

What Qualifies as a Special Enrollment Period Under the ACA?

A Special Enrollment Period qualifies when a person experiences specific events that change eligibility or access to coverage, including loss of health insurance, household changes, residence changes, and other special circumstances such as changes in immigration or incarceration status. The Marketplace treats each qualifying life event as a hyponym under the broader hypernym of insurance enrollment periods; for example, loss-of-coverage SEP is a hyponym of SEP generally. Typical documentation that proves a QLE includes termination letters, birth certificates, marriage certificates, proof of new residence, and government documents indicating changes in lawful presence. Knowing which document matches which event speeds pre-enrollment verification and avoids requests for additional proofs that prolong processing. The following subsection explains how timing and duration differ between SEPs and the Open Enrollment Period, including the standard 60-day rule and notable exceptions.

How Does SEP Timing and Duration Work Compared to Open Enrollment?

SEP timing is centered on a 60-day special enrollment period that generally starts from the date of the qualifying life event or the date the person becomes aware of the event, whereas Open Enrollment has fixed calendar dates each year such as open enrollment 2026 baseline windows. The 60-day period gives individuals a clear application window, but exceptions exist—for example, some Medicaid loss SEP cases or state-specific rules may allow different windows or retroactive enrollment in certain situations. Coverage effective dates after SEP enrollment depend on the event type and application date; births and adoptions often permit immediate or retroactive coverage, while loss of employer coverage commonly results in coverage starting the first day of the month after plan selection and payment. Understanding these timing rules clarifies action steps: gather proofs promptly, submit applications early in the 60-day period, and track payment deadlines to set effective dates. The next main section catalogs which qualifying life events most commonly trigger SEP eligibility and the documentation each typically requires.

| Enrollment Period | Timing | Eligibility Triggers | Typical Duration |

|---|---|---|---|

| Special Enrollment Period (SEP) | Event-driven; 60 days from QLE in most cases | Qualifying life events (loss of coverage, household changes, moves, special cases) | Standard: 60 days; exceptions vary by state/event |

| Open Enrollment Period (OEP) | Annual calendar window (e.g., Nov–Jan for 2026 baseline) | Open to anyone without needing a QLE | Fixed annual duration (dates set each year) |

| Medicaid/CHIP Enrollment | Continuous in many states; some loss-based windows | Eligibility based on income and household; loss of Medicaid may trigger SEP | Varies; some states allow extended windows or retroactive coverage |

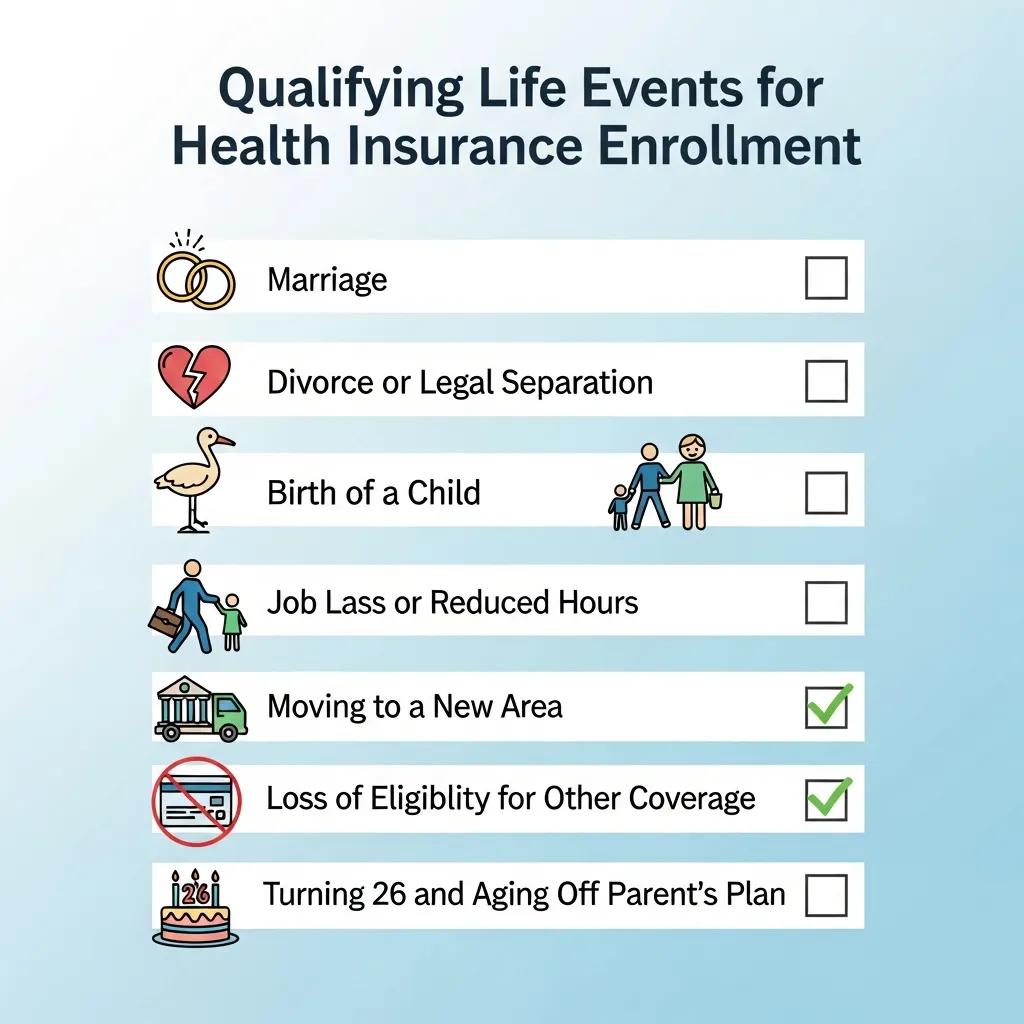

Which Qualifying Life Events Make You Eligible for a Special Enrollment Period?

Which qualifying life events make you eligible for a Special Enrollment Period centers on categories such as loss of coverage, household changes, residence changes, and other specialized cases like citizenship changes or leaving incarceration. Each QLE category maps to specific documentation expectations and timing rules, and the Marketplace evaluates the event type to assign the appropriate 60-day window or exception. The following subsections break down loss-of-coverage events and household changes, providing examples, proof types, and immediate steps to take to preserve subsidy eligibility. Knowing these grouped events helps people recognize eligibility quickly and avoid gaps in coverage.

What Loss of Coverage Events Trigger SEP Eligibility?

Loss of coverage events that qualify include involuntary termination of employer-sponsored insurance, aging off a parent’s plan at 26, losing Medicaid or CHIP, and coverage lapses due to nonpayment or plan cancellations. To prove a loss-of-coverage SEP, commonly accepted documents include a termination letter from an employer or insurer, a notice of Medicaid/CHIP termination, or an aged-off notice indicating your dependent status ended on a specific date. Timing is crucial: submit your application early in the 60-day special enrollment period and be prepared to show the exact date coverage ended to determine effective dates and eligibility for premium tax credits. If you receive notice in advance of a loss (like a scheduled employer coverage end), you may be able to enroll before coverage ends, which minimizes the uninsured gap. The next subsection explains household changes—marriage, birth, adoption, or divorce—and how they affect SEP eligibility and subsidy recalculation.

This policy brief details how individuals can maintain health coverage during significant life transitions, emphasizing the importance of proactive enrollment strategies.

Health Coverage During Life Transitions: Maximizing Enrollment

This policy brief is the third in a series discussing seamless health care coverage for individuals undergoing work or life transitions.[1] The brief summarizes past research on the prevalence of loss of coverage due to life transitions and the importance of using existing institutions to inform and enroll people. It also describes California legislation and programs that have been adopted to connect people into coverage. Finally, the brief identifies remaining gaps in coverage for selected target groups and provides specific recommendations on how to maximize enrollment in Covered California for individuals undergoing work or life transitions.Maximizing health insurance enrollment through Covered California during work and life transitions, 2015

How Do Household Changes Affect SEP Eligibility?

Household changes that trigger SEPs include marriage, divorce, birth, adoption, placement in foster care, and death of a household member; these events may change the size of the tax household and therefore affect premium tax credits and cost-sharing reductions. Documentation examples include marriage certificates, birth or adoption certificates, court orders for foster placement, and death certificates when applicable; the Marketplace will use these documents to update household size and recompute subsidies as needed. When household composition changes, prompt reporting ensures subsidy calculations reflect the new income-per-person ratio, which can increase or decrease premium tax credits; this can materially change monthly payments and plan selection strategy. Immediate next steps are to update your Marketplace application, submit required proofs, and review plan coverage for any dependents added or removed from your household. The next major section covers how moving or changing residence affects SEP eligibility and plan availability by ZIP code or county.

| Qualifying Event (QLE) | Examples | Documentation | Deadline Notes |

|---|---|---|---|

| Loss of Coverage | Job loss, aging off at 26, losing Medicaid | Termination letter, aged-off notice, Medicaid termination notice | Standard: 60 days from loss; some states vary |

| Household Change | Marriage, birth, adoption, divorce | Marriage certificate, birth certificate, adoption paperwork, divorce decree | 60 days from event; birth/adoption may allow special effective dates |

| Residence Change | Moving across ZIP/county/state lines | Lease, utility bill, driver's license, change-of-address form | 60 days from move; moving across state lines may affect Marketplace |

| Special Cases | Citizenship change, release from incarceration, tribal enrollment | Immigration papers, release documents, tribal enrollment letter | Documentation critical; timing rules may differ |

How Does Moving or Changing Residence Impact Your Special Enrollment Period Eligibility?

Moving or changing residence can create SEP eligibility because coverage options and plan networks are location-specific; moving into a new service area typically qualifies as a QLE that opens a 60-day special enrollment period to select plans available in the new ZIP code or county. The mechanism is straightforward: residence change → change in available plans/networks → SEP eligibility to enroll in local Marketplace plans. Acceptable proofs of a move commonly include a signed lease, utility bills in your name at the new address, a driver’s license with updated address, or a change-of-address confirmation from the postal service; students and temporary relocations may require additional context to validate intent to reside. Because plan availability and provider networks vary by county, a move can immediately affect which providers are in-network and which drug formularies apply, so compare plan networks and pharmacy coverage as soon as you become eligible. The next subsections cover documentation nuances for moves and how ZIP/county changes affect plan choices so you can prepare both proofs and comparison checklists.

What Documentation Is Needed When You Move to a New Service Area?

When you move to a new service area, acceptable proofs of residence usually include a signed lease or rental agreement, recent utility bills showing your new address, a driver's license or state ID updated to the new address, or a change-of-address confirmation. For temporary moves—such as students or short-term work assignments—documentation that shows intent to reside, like a student housing agreement or employer letter, may be accepted; alternate proofs can help if primary documents are not yet available. Uploading clear scans or photos of these documents during the Marketplace verification process reduces back-and-forth requests and speeds plan selection within your 60-day window. Keep in mind that documentation requirements can vary slightly by state Marketplace, so gather multiple types of proof if possible to avoid delays. The following subsection explains how changing ZIP code or county affects which plans and providers you can choose.

How Does Changing ZIP Code or County Affect Available Health Plans?

Changing ZIP code or county can change plan availability because insurers offer different networks, premiums, and formularies by service area, meaning your current plan may not be available or may be out-of-network after a move. When your ZIP or county changes, perform a quick plan comparison focused on three priorities: provider network continuity, prescription drug coverage, and total estimated out-of-pocket costs for your typical care. If your current primary care provider is out-of-network in the new area, consider plans with a sufficiently broad network or choose a new provider and evaluate referral and specialist access. A short checklist helps guide immediate actions: confirm network participation, compare premiums plus deductibles, and review formulary coverage for essential medications. The next main section expands coverage to other life changes that can trigger SEPs such as income shifts, citizenship changes, and release from incarceration.

What Other Life Changes Qualify You for a Special Enrollment Period?

Other life changes qualify for SEPs beyond loss-of-coverage and household moves; these include significant income changes affecting subsidy eligibility, gaining or losing lawful presence such as amended immigration status, release from incarceration, experiences of domestic violence, and recognition of tribal membership. These special SEP cases often require specific government documents—immigration paperwork, release certificates, tribal enrollment letters—and timing rules may allow retroactive or immediate coverage depending on the event. Income shifts are particularly important because they affect premium tax credits and cost-sharing reductions; reporting income changes promptly keeps your monthly premium aligned with your eligibility. The next subsections look at income-driven SEP triggers and the documentation and timing for special cases like citizenship changes or leaving incarceration, so you can respond accurately when these circumstances arise.

How Do Income Changes Affect SEP Eligibility and Subsidy Access?

Significant income changes—such as losing a job, starting a new job with different pay, or changes in household composition—can alter eligibility for premium tax credits and cost-sharing reductions and may trigger a Special Enrollment Period if they create a new eligibility category. The Marketplace uses household income and size to calculate premium tax credits, so increasing or decreasing income per person will change the subsidy amount; a simple example: if household income drops, the same benchmark plan becomes more affordable due to higher premium tax credits. Report income changes promptly by updating your application and submitting pay stubs, employer letters, or unemployment award letters as evidence; doing so can result in immediate subsidy recalculation and a lower monthly premium. Retroactive adjustments are possible in some cases when income changes are proven, but prospective reporting is the primary mechanism to avoid coverage gaps and unexpected year-end tax reconciliations. The next subsection addresses how special SEP cases like gaining citizenship or leaving incarceration are handled.

What Are Special SEP Cases Like Gaining Citizenship or Leaving Incarceration?

Special SEP cases—such as gaining citizenship, acquiring lawful presence, release from incarceration, or recognition as a tribal member—have unique documentation and timing requirements and may allow enrollment outside the normal 60-day structure depending on program rules. Typical documents include naturalization certificates, immigration status change notifications, official release documentation from correctional facilities, and tribal enrollment verification letters; these documents establish eligibility changes that the Marketplace and other programs recognize. Timing and effective dates can vary: some citizenship or lawful-presence changes allow immediate Marketplace enrollment, while incarceration-release cases may trigger special handling to reduce uninsured time after release. Because these events often involve separate government agencies, coordinating document submission and verifying details with the Marketplace or a qualified assister can materially speed effective coverage. The next section describes how to apply for a Special Enrollment Period through the Health Insurance Marketplace with a detailed how-to.

How Do You Apply for a Special Enrollment Period Through the Health Insurance Marketplace?

Applying for a Special Enrollment Period through the Health Insurance Marketplace follows a stepwise process: confirm your qualifying life event, gather required documentation, log into or create a Marketplace account, submit the SEP application with proofs, and select and pay for a plan before the SEP window closes. The application mechanism uses the Marketplace platform to verify event documentation and determine subsidy eligibility, and pre-enrollment verification may require uploading scanned documents or mailing proofs to the Marketplace depending on your state’s procedures. Knowing the step-by-step process reduces errors: prepare documents before you begin, ensure names and dates match across proofs, and respond promptly to any follow-up verification requests to avoid delays in plan effective dates. The next subsections provide a numbered HowTo for SEP enrollment and a per-QLE document checklist to help you complete submissions correctly during the 60-day special enrollment period.

What Are the Step-by-Step Instructions for SEP Enrollment?

- Confirm Eligibility: Identify the qualifying life event and the date it occurred to determine your SEP window.

- Gather Documents: Collect primary and secondary proofs relevant to your QLE, ensuring names and dates match across documents.

- Access Marketplace Account: Log in to your existing Marketplace account or create a new one to start the SEP application.

- Submit SEP Application: Complete the SEP-specific application fields, upload your documents, and answer verification questions accurately.

- Select and Pay for a Plan: Choose a plan available in your service area, confirm subsidy eligibility, and make the initial payment if required to set an effective date.

Which Documents Are Required to Prove Your Qualifying Life Event?

Required documents vary by QLE but follow a predictable pattern of primary proofs and acceptable alternates; primary proofs include employer termination letters, birth or marriage certificates, signed leases, and official government notices for immigration or incarceration release. Acceptable alternates might include pay stubs showing job loss timing, a hospital birth record, or a notarized affidavit when standard documents are unavailable; offering multiple corroborating documents often expedites verification. When uploading documents to the Marketplace, ensure scans are legible, include identifying names and dates, and redact sensitive information not required for verification; secure upload methods protect personal data during the process. If you expect delays gathering official documents, contact a Marketplace assister or certified agent to discuss acceptable secondary proofs and timelines so your SEP window is preserved. After verification guidance, the next section covers important deadlines and coverage start dates, including the interaction with open enrollment 2026 and the January 15 ACA deadline.

For readers who need immediate help navigating these steps: our content intent is Educational, generate business leads. If you prefer hands-on assistance with documentation, plan selection, and timely submission during your SEP, qualified enrollment experts can provide one-on-one guidance to compile proofs and complete Marketplace steps quickly. These services emphasize educational support and practical enrollment execution for applicants who want to minimize errors and secure coverage within their SEP window. To explore personalized assistance, look for credentialed local assisters, certified brokers, or enrollment experts who specialize in Marketplace SEP processes and documentation verification.

What Are the Important Deadlines and Coverage Start Dates for Special Enrollment Periods?

Important deadlines for Special Enrollment Periods typically center on the 60-day special enrollment period window following a qualifying life event, while Open Enrollment Period dates—such as the ACA enrollment deadlines 2026 baseline—set annual access for anyone without a qualifying event. For 2026, many Marketplaces use baseline Open Enrollment dates beginning in early November and using a January 15 ACA deadline to finalize plan enrollments, but SEP windows operate independently of those calendar OEP dates. Coverage effective dates after SEP enrollment depend on event type and timing: applications submitted before the first day of the month, with payment, often result in coverage effective the first of the next month; births or adoptions may allow immediate or retroactive coverage. State-specific exceptions exist, particularly for Medicaid loss SEP cases where some states allow extended windows (e.g., 90 days) or retroactive enrollment, so understanding your state’s rules is essential to set expectations. The next subsections break down how the 2026 enrollment calendar interacts with SEP timing and provide concrete examples of coverage start dates.

How Do 2026 ACA Enrollment Deadlines Affect SEP Applications?

Open Enrollment Period dates for 2026 create a baseline context—many consumers aim to complete enrollment by the January 15 ACA deadline—yet SEPs remain event-driven and can occur before, during, or after the OEP window depending on the qualifying life event date. If a qualifying event occurs close to OEP dates, you may have overlapping options: you can use SEP rules if the event qualifies or rely on OEP if you prefer different plan options that open November through mid-January; both paths affect subsidy calculations similarly when you report income and household details. State exceptions may change SEP timing; for example, losing Medicaid in some states triggers specialized Medicaid loss SEP rules that differ from the standard 60-day window. Practical example: if you lose employer coverage on December 20, you generally have 60 days from that date to enroll through SEP, but you should act quickly to secure a plan effective as soon as possible to avoid a lapse in coverage. The next subsection explains typical coverage effective date rules after SEP enrollment.

When Does Coverage Begin After SEP Enrollment?

Coverage effective dates after SEP enrollment typically follow a rule where enrollment and required payment submitted by the Marketplace deadline result in coverage starting the first day of the month after plan selection, but exceptions exist for certain events such as birth or adoption where coverage can begin immediately or retroactively to the date of the event. For example, enrolling and paying on the 10th of a month may produce a first-of-next-month effective date, while newborns added through SEP processes can sometimes have coverage effective on the date of birth pending verification. Timing often hinges on prompt payment of initial premiums; failure to pay by the plan’s deadline can delay the effective date. Always check verification notices from the Marketplace and follow up quickly on any requests for additional documentation to protect your anticipated effective date. The next major section addresses common questions people have about SEPs and clarifies typical misconceptions.

| Event Type | Application Window | Typical Coverage Effective Date / Notes |

|---|---|---|

| Loss of Employer Coverage | 60 days from loss (standard SEP) | Coverage often begins first of next month after enrollment and payment |

| Birth or Adoption | 60 days from event (special handling) | May be effective retroactively to birth/adoption date in many cases |

| Move to New Service Area | 60 days from move | Coverage begins depending on enrollment/payment timing; plan networks change by ZIP |

| Medicaid Loss SEP | Varies (some states extend to 90 days) | State rules may allow retroactive coverage or extended windows |

What Are Common Questions About Special Enrollment Periods?

People commonly ask whether they can get health insurance after Open Enrollment ends, how long a Special Enrollment Period lasts, and what to do if they lack typical documentation; answering these PAA-style questions directly reduces confusion and supports faster action. Short, focused answers enable readers to determine next steps quickly and link to deeper sections in this article for documentation checklists, timelines, and example scenarios. The following subsections provide concise answers to common queries—yes/no answers followed by brief contextual explanation—and introduce actions to take so readers feel empowered to proceed. After these clarifications, a short call to action offers educational assistance and options for expert help if needed.

Can You Get Health Insurance After Open Enrollment Ends?

Yes — you can get health insurance after Open Enrollment ends if you experience a qualifying life event that triggers a Special Enrollment Period, such as losing employer coverage, getting married, having a baby, or moving to a new service area. This mechanism ensures that people who experience life changes that affect their insurance access are not forced to wait until the next annual Open Enrollment and risk a gap in coverage. To act, identify your qualifying event, confirm the event date, gather documentation, and submit your SEP application promptly within your 60-day special enrollment period. If you do not have a qualifying event, your next chance to enroll through Marketplace plans is the following Open Enrollment Period unless you qualify for Medicaid/CHIP or another program with continuous enrollment. The next subsection answers how long a typical SEP lasts and how to calculate your window.

How Long Does a Special Enrollment Period Last?

A Special Enrollment Period typically lasts 60 days from the qualifying life event date, although some specific scenarios and state rules create exceptions that extend or alter the window—for example, certain Medicaid loss cases in some states may allow 90 days or different retroactive options. Start counting your SEP window from either the date the qualifying event occurred or, in some cases, the date you were notified of the event; if you receive an advance notice of coverage loss, your window might begin before the actual loss date, allowing you to enroll proactively. To calculate your SEP window, mark the event date, add 60 calendar days, and plan to submit documentation and select a plan early in that period to avoid last-minute verifications. Prompt action also improves your chances of obtaining an earlier coverage effective date by minimizing processing time.

For readers who want direct assistance resolving documentation questions or completing SEP submissions: our approach is Educational, generate business leads. If you prefer help compiling evidence, choosing plans that preserve provider access, and submitting SEP paperwork accurately to protect your coverage start date, qualified enrollment experts can provide guided support and hands-on troubleshooting. These services focus on education plus practical enrollment support to minimize processing delays, preserve subsidy eligibility, and reduce the risk of coverage gaps.

How Can You Find the Right Health Insurance Plan During a Special Enrollment Period?

Finding the right health insurance plan during a Special Enrollment Period requires balancing network access, premiums, deductibles, prescription coverage, and subsidy impacts tied to household income. The decision mechanism involves matching health needs and budget constraints to plan attributes, where premium tax credits and cost-sharing reductions may shift after household or income changes. Use a prioritized checklist to compare plans quickly during the 60-day special enrollment period, focusing first on provider continuity, second on total annual costs (premiums plus expected out-of-pocket expenses), and third on prescription formularies and specialist access. If you prefer a guided process, enrollment experts can help analyze trade-offs and recommend plans that preserve access to necessary providers while aligning with subsidy eligibility. The next subsections offer a detailed checklist for choosing Marketplace plans and describe the value enrollment experts can add when time is limited.

What Should You Consider When Choosing a Marketplace Plan During SEP?

- Provider Network: Confirm that your primary care physician and key specialists are in-network under the new plan.

- Total Cost: Compare monthly premiums plus expected deductibles, copays, and maximum out-of-pocket expenses for your typical care.

- Prescription Coverage: Verify that essential medications are on the plan’s formulary and note tier placement and copayment amounts.

- Subsidy Impact: Review how updated household income or size affects premium tax credits and select plans that optimize net monthly cost.

- Service Area: Check whether the plan’s network and pharmacy coverage align with your new ZIP code or county if you moved recently.

After checking these factors, prioritize plans that minimize disruption to ongoing care while delivering predictable costs. The next subsection identifies specific ways health insurance experts can help you navigate SEP enrollment and plan selection efficiently.

How Can Health Insurance Experts Help You Navigate SEP Enrollment?

Health insurance experts—certified assisters, brokers, or enrollment counselors—help by clarifying eligibility, identifying acceptable documentation for your qualifying life event, comparing plan networks and total costs, and submitting SEP applications correctly to the Marketplace. Their assistance matters most when time is short during a 60-day special enrollment period, when documentation is nonstandard, or when household income changes complicate subsidy calculations. Experts can also model simple subsidy scenarios to show how changes in income or household size affect premium tax credits and out-of-pocket exposure, enabling informed decisions under pressure. For readers who want hands-on help assembling documentation, selecting plans quickly, and ensuring verification requests are addressed promptly: our content intent is Educational, generate business leads, and experts offering enrollment assistance can provide targeted, educational support that accelerates successful SEP completion.

Key ways experts assist include:

- Reviewing and organizing required proofs for Marketplace verification.

- Comparing plan networks and financial trade-offs tailored to your care needs.

- Submitting SEP applications and monitoring verification responses to avoid processing delays.

| Event (Entity) | Attribute (Application window) | Value (Coverage effective date / notes) |

|---|---|---|

| Loss of employer coverage | 60 days from loss | Coverage effective generally first of next month after enrollment/payment |

| Move to new service area | 60 days from move | Coverage effective depends on enrollment timing; plan networks change by ZIP |

| Birth or adoption | 60 days from event (special handling) | Coverage may be retroactive to birth/adoption date if verified |

| Income change affecting subsidies | Varies (report promptly) | Subsidies recalculated prospectively; potential retroactive adjustments in specific cases |

Immediate checklist for SEP action:

- Gather primary proofs (termination letters, certificates, lease) and backups.

- Start your Marketplace application early in the 60-day window to permit verification time.

- Compare plans with a focus on provider continuity, total cost, and drug coverage.

References

- California HealthCare Foundation. (2015). Maximizing Health Insurance Enrollment Through Covered California During Work and Life Transitions. Policy Brief. ↩

A Special Enrollment Period (SEP) lets you enroll in ACA-compliant health coverage outside the annual Open Enrollment when you experience certain qualifying life events, such as losing employer...