Ben J. Mauldin | Feb 21 2026 01:43

If you're a family living in Lexington or anywhere in South Carolina and you don't have health insurance through an employer or Medicare, the ACA Marketplace — also called Obamacare — is probably the most important resource you haven't fully explored. The truth is, most South Carolina families qualify for significant financial help, and many are leaving hundreds or even thousands of dollars on the table every year because they simply don't know where to start.

At Mauldin Insurance Group, we help Lexington families navigate the ACA marketplace every day. This guide is designed to answer the questions we hear most often, cut through the confusion, and help you understand what coverage is available, what it actually costs, and exactly how to get help.

| ✅ Quick Takeaway If your household earns between 100% and 400% of the Federal Poverty Level — or even above that with the expanded subsidies now in place — you may qualify for premium tax credits that dramatically reduce what you pay for health insurance each month. Many Lexington families pay less than $50/month for solid ACA coverage. |

What Is ACA Health Insurance?

The Affordable Care Act (ACA), signed into law in 2010, created the Health Insurance Marketplace — a system where individuals and families can shop for and enroll in private health insurance plans. Unlike employer plans, ACA plans are purchased directly by individuals, and the government offers financial assistance in the form of premium tax credits to help make coverage affordable.

In South Carolina, residents use HealthCare.gov to compare and enroll in ACA plans. The state did not create its own exchange, so all plans are administered through the federal marketplace — but the options, prices, and subsidies are the same.

All ACA plans must cover ten essential health benefits by law, including:

- Preventive care and screenings (often at no additional cost)

- Emergency services and hospitalization

- Prescription drug coverage

- Mental health and substance use disorder services

- Maternity and newborn care

- Pediatric services including dental and vision for children

- Lab tests and rehabilitative services

2026 ACA Subsidy Guide for South Carolina Families

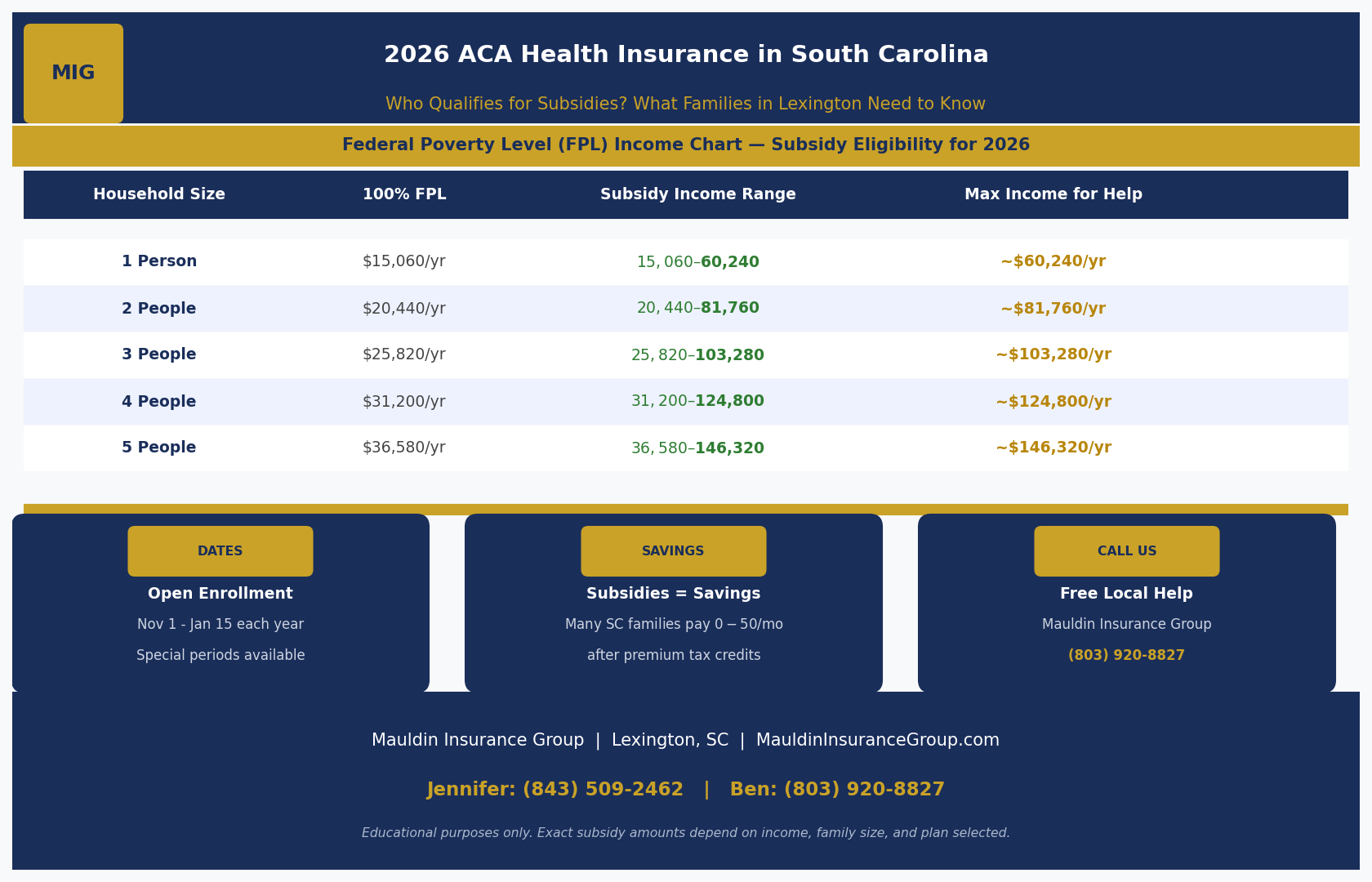

The most powerful feature of ACA plans is the premium tax credit — a subsidy that reduces your monthly premium. Whether and how much you receive depends on your household income relative to the Federal Poverty Level (FPL). Here is how that looks for 2026 in South Carolina:

| Household Size |

100% FPL (Annual) |

Subsidy Eligibility Range |

Max Income for Help |

| 1 Person |

$15,060 |

$15,060 – $60,240 |

~$60,240 |

| 2 People |

$20,440 |

$20,440 – $81,760 |

~$81,760 |

| 3 People |

$25,820 |

$25,820 – $103,280 |

~$103,280 |

| 4 People |

$31,200 |

$31,200 – $124,800 |

~$124,800 |

| 5 People |

$36,580 |

$36,580 – $146,320 |

~$146,320 |

Note: These income figures are approximate and based on 2026 FPL guidelines. The "subsidy range" refers to the income band in which premium tax credits are available. Families above 400% FPL may still qualify for some assistance under the enhanced subsidies that have been extended — we can run your specific numbers in a free consultation.

| 💡 Important: South Carolina Did Not Expand Medicaid Unlike many states, South Carolina has not expanded Medicaid under the ACA. This means that adults with incomes below 100% of the FPL — roughly $15,060 for a single person — may fall into what's called the "coverage gap" and may not qualify for ACA subsidies or Medicaid. If this applies to you, contact us and we will help you explore every option available. |

The Four ACA Metal Tiers: Which Plan Is Right for Your Family?

ACA plans come in four tiers — Bronze, Silver, Gold, and Platinum — named for the percentage of costs the plan covers. Understanding these tiers is the key to choosing wisely.

Bronze Plans

Bronze plans have the lowest monthly premiums but the highest out-of-pocket costs when you use care. They are generally best for people who are young, healthy, and primarily want protection against a catastrophic event. The plan covers roughly 60% of costs; you pay 40%.

Silver Plans

Silver plans are the most popular choice for subsidy-eligible families, and for good reason. Not only do they qualify for premium tax credits, but Silver plans are the only tier eligible for Cost-Sharing Reductions (CSRs) — additional savings that lower your deductibles, copays, and out-of-pocket maximums if your income qualifies. For many Lexington families, a Silver plan with CSRs delivers the best overall value.

Gold Plans

Gold plans have higher premiums but lower out-of-pocket costs when you use care. The plan covers roughly 80% of costs. These are ideal for families who anticipate using health services frequently throughout the year — managing chronic conditions, regular specialist visits, or ongoing prescriptions.

Platinum Plans

Platinum plans have the highest premiums and the lowest out-of-pocket costs (covering about 90%). They are designed for people who expect very high healthcare utilization and want maximum predictability in their costs.

| 🏡 A Lexington Family Example Consider a family of four in Lexington with a combined household income of $70,000 per year. Based on 2026 guidelines, they would fall within the subsidy-eligible range and could receive a substantial premium tax credit — potentially reducing their Silver plan premium from over $1,200/month to $200–$400/month or less, depending on their specific plan selection. That is a savings of $9,600 or more per year. |

When Can You Enroll? Open Enrollment and Special Enrollment Periods

You cannot enroll in an ACA plan just any time of year. There are specific windows when enrollment is allowed.

Open Enrollment Period (OEP)

The annual Open Enrollment Period for 2026 coverage runs from November 1 through January 15. To have coverage that begins on January 1, you must enroll by December 15. Plans enrolled after December 15 and by January 15 take effect February 1.

Special Enrollment Periods (SEPs)

If you experience certain qualifying life events outside of Open Enrollment, you may be eligible for a Special Enrollment Period. These include:

- Losing job-based health coverage (including COBRA expiration)

- Getting married or divorced

- Having a baby, adopting a child, or placing a child for adoption or foster care

- Moving to a new address in a different coverage area

- A change in household income that affects your subsidy eligibility

- Aging off a parent's plan at 26

SEPs typically give you 60 days from the qualifying event to enroll. Don't wait — contact us and we can help you document your qualifying event and secure coverage quickly.

Understanding Your ACA Plan Costs: It's More Than Just the Premium

Many people focus only on the monthly premium when comparing plans, but there are several cost components that determine your total out-of-pocket spending throughout the year:

- Premium: The amount you pay each month for coverage, reduced by any tax credits you receive.

- Deductible: The amount you pay out of pocket before your insurance starts covering certain costs.

- Copays and Coinsurance: Fixed or percentage costs you pay for specific services even after meeting the deductible.

- Out-of-Pocket Maximum: The most you will ever have to pay in a plan year. After hitting this limit, your plan covers 100% of covered services.

In 2026, the out-of-pocket maximum for ACA plans is capped at $9,450 for individuals and $18,900 for families. This is an important protection — it means even in a worst-case health scenario, your costs are limited.

ACA Insurance for Self-Employed and Small Business Owners in Lexington

If you're self-employed, a freelancer, a gig worker, or a small business owner in Lexington or the Midlands area, you are exactly who the ACA Marketplace was designed for. Without an employer providing group coverage, you bear the full cost of health insurance — but you also have full access to all available subsidies.

As a self-employed individual, your ACA income is based on your net self-employment income (after business deductions), which means your actual subsidy eligibility may be more favorable than you think. Additionally, self-employed individuals can deduct 100% of their health insurance premiums from their federal income taxes, separate from the premium tax credit.

For small business owners with employees, we can also discuss group health insurance options through the SHOP Marketplace, which may offer additional tax credits for qualifying small employers.

How Mauldin Insurance Group Helps Lexington Families with ACA Coverage

Shopping for health insurance on HealthCare.gov alone can feel overwhelming — dozens of plans, confusing terminology, and the fear of choosing the wrong one and facing unexpected costs. That's where we come in.

As an independent insurance agency based right here in Lexington, South Carolina, Mauldin Insurance Group works with multiple carriers to find you the best plan for your specific situation. Here's what working with us looks like:

- We start with a free, no-pressure consultation — by phone, video, or in person.

- We review your household income, expected healthcare needs, and preferred doctors.

- We compare every available plan in your area — not just the ones that pay us more.

- We calculate your exact subsidy amount so there are no surprises.

- We walk you through enrollment step by step.

- We stay with you all year for questions, claims help, and annual reviews.

| 📞 Ready to Find Out What You Qualify For? Call or text Ben Mauldin at (803) 920-8827 or Jennifer Mauldin at (843) 509-2462. You can also reach us at MauldinInsuranceGroup.com. There's no cost and no obligation — just honest answers from a local team that genuinely cares about South Carolina families. |

Frequently Asked Questions: ACA Health Insurance in South Carolina

Does it matter that South Carolina didn't expand Medicaid?

Yes, it matters if your income falls below 100% of the Federal Poverty Level. Adults in this income range may fall into a "coverage gap" where they earn too little for ACA subsidies but don't qualify for Medicaid under SC's current rules. If you are in this situation, contact us — there may be other options available to you, and we stay current on any state-level changes.

Can I keep my current doctors with an ACA plan?

It depends on the plan. Each ACA plan has a network of in-network providers. Before enrolling, we always verify that your preferred primary care physicians and specialists are included in the plan's network. Choosing out-of-network providers typically means paying significantly more.

What if my income changes during the year?

Report any income changes to HealthCare.gov as soon as possible. Changes in income can affect your subsidy amount, either increasing or decreasing it. Failing to report changes can result in a tax bill or repayment of excess credits when you file your taxes.

Is there a penalty for not having ACA insurance?

There is no longer a federal penalty for not having ACA coverage. However, South Carolina does not have a state-level individual mandate either. That said, going uninsured carries significant financial risk — one hospitalization can cost tens of thousands of dollars without coverage.

Can I get ACA insurance if I'm self-employed?

Absolutely. Self-employed individuals and freelancers are among the most common users of ACA Marketplace plans. Your eligibility for subsidies is based on your projected net self-employment income for the year. We help self-employed clients estimate income and maximize subsidy eligibility regularly.

Can my children and I be on an ACA plan together?

Yes. ACA plans cover families, and children can be covered on a family plan up to age 26. Plans cover all children regardless of health status — no child can be denied coverage or charged more due to a pre-existing condition.

The Bottom Line for Lexington Families

ACA health insurance in 2026 offers South Carolina families a real, affordable path to quality health coverage. With the subsidy system that caps what you pay based on your income, many families in Lexington and the greater Columbia area can access coverage they thought was out of reach.

The key is having someone in your corner who understands the system and takes the time to find the best fit for your specific situation. That's exactly what Mauldin Insurance Group is here to do.

Don't go it alone. Let us run your numbers, compare your options, and walk you through enrollment — at no cost to you.

| Mauldin Insurance Group Independent Insurance Agency 100 Old Cherokee Rd STE F #167 Lexington, SC 29072 |

Jennifer: (843) 509-2462 Ben: (803) 920-8827 Text: (803) 848-9461 MauldinInsuranceGroup.com |

This article is for educational purposes only and does not constitute legal or financial advice. Coverage options and subsidy amounts are subject to change. Contact us for personalized guidance.

If you're a family living in Lexington or anywhere in South Carolina and you don't have health insurance through an employer or Medicare, the ACA Marketplace — also called Obamacare — is probably...